Divided on Dividends

Many investors and pundits love dividends, but does this popular opinion hold up? First, let us review the pros and cons of dividends.

Pros:

- Provide a regular and growing (hopefully more than inflation) source of cash.

- Hold management to more disciplined capital allocation decisions.

- Provide psychological comfort helping investors stay invested during downturns.

- Research suggests dividend stocks exhibit lower shareholder turnover1 & volatility.

Cons:

- Dividends are not free. They are a transfer of value, not “passive income” as the finfluencers would have you believe. When a company pays $1 in dividends, its share price typically drops by about $1.

- Tax inefficient due to being taxed in the year dividends are received, reducing compounding while capital gains can be deferred indefinitely. Investors also lose control over when they realize taxes.

- Dividends take away from growth reinvestment or other capital allocation decisions.

- High dividend yields can be value traps and dividend cuts can be sudden which lead to stock price declines, signaling a sign of distress.

- Sector and style concentration risk due to dividends clustering in financials, utilities, energy, and telecoms. Lack of diversification can expose investors to interest rate risk, regulatory risk, and sector/style-specific drawdowns.

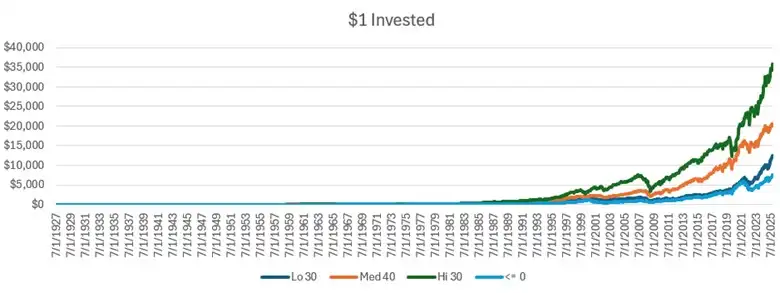

Now that we have discussed the qualitative, what does the data tell us? The data below was obtained from The Center for Research in Security Prices, LLC (CRSP) and compiled by Ken French. Since 1927, the top 30% high dividend stock index outperformed the bottom 30%, as well as the no dividend (<=0%) stocks.

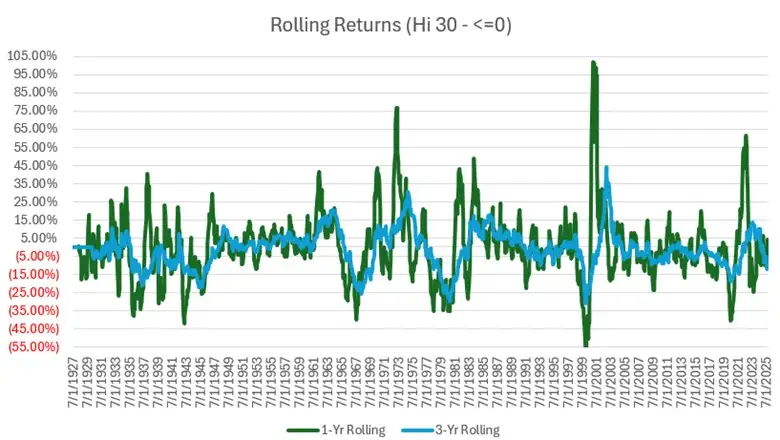

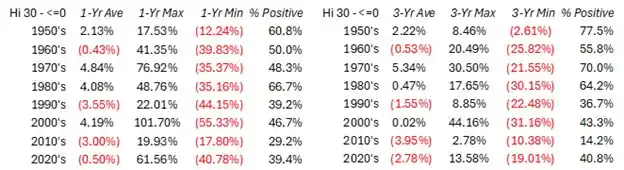

Mystery solved? High dividend stocks win. Dividends can feel safe and attractive and a wise financial advisor once said, a coupon in the hand is worth more than two in the bush. Unfortunately, the answer is not so simple. Over various decades, the performance of high-dividend stocks has swung wildly and in the modern era, the “dividend premium” has vanished. The information below shows this variability using rolling returns (trailing 1 and 3 year returns for every month) and a table of returns by decade. To calculate the returns, I take the monthly returns for the highest 30% of dividend paying stocks and subtract the return of stocks that pay no dividends. Along with the return variations, the popularity of dividends among corporations has varied over time. More than 80% of the largest 1500 stocks paid dividends in the 1970s, and the fraction declined constantly to about 50% in the 2000s.2 When you look at the Russell 3000 index, dividends currently make up 60% of the eligible universe by number and about 20% of the total market capitalization.3 Investors limiting themselves to dividend stocks ignore a large universe of investment opportunities.

I decided to dig deeper and ask if the dividend was the main reason for yielding returns greater than the market. I turned to Larry Swedroe’s research (2023) on the topic. Yin Chen and Roni Israelov confirmed and expanded on Swedroe’s work with their paper Income Illusions (2024), which was published in the Journal of Asset Management. Both research papers find that once investors account for quantitative risk factors, high-dividend stock returns become statistically insignificant to negative. The historical dividend outperformance is largely explained by exposures to various factors such as value (low price-to-book), quality (profitability), and defensive factors (low volatility and conservative investment) rather than dividend yield. Said differently, research shows that investors could benefit by directly targeting factor exposures rather than simply using a dividend screen.

In conclusion, the data does warn against assuming dividends help returns. Dividends can be useful but are often over-hyped. No single investment strategy guarantees higher returns in all market environments and all time periods. Maintaining a diversified and balanced portfolio is the best bet you can make. There is nothing stopping you from making your own dividend by selling stock periodically.

Read the May 2026 Financial Planning Focus:

- "Something Old, New, Borrowed, Blue and…." by Laurie Kramer, CFP® and Kristan Anderson, CEBS®, CFP®

- "Is a Trump Account Right for Your Child?" by Victoria G. Henry, CFP®

- "From Fear to Freedom: Mastering Your Finances in Retirement" by Laura Nash, CFP®

Sources

2NDVR - Income Illusions: Challenging the High Yield Stock Narrative

3The Evidence Against Favoring Dividend-Paying Stocks

Data Definitions

- The 5-Factor Fama-French model, include the market (MKT), size factor (SMB), value factor (HML), profitability factor (RMW), and investment (CMA).

- Momentum factor (UMD) and a defensive factor (BAB), are from the AQR Data Library.

West Financial Services, Inc. (“WFS”) offers investment advisory services and is registered with the U.S. Securities and Exchange Commission (“SEC”). SEC registration does not constitute an endorsement of the firm by the SEC nor does it indicate that the firm has attained a particular level of skill or ability. You should carefully read and review all information provided by WFS, including Form ADV Part 1A, Part 2A brochure and all supplements, and Form CRS.

Certain information contained herein was derived from third party sources, as indicated, and has not been independently verified. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any information presented. Where such sources include opinions and projections, such opinions and projections should be ascribed only to the applicable third party source and not to WFS.

This information is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product, security, or concept. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. You should not treat these materials as advice in relation to legal, taxation, or investment matters. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisers.