Financial Planning Focus – Health Savings Accounts as Supplemental Retirement Savings

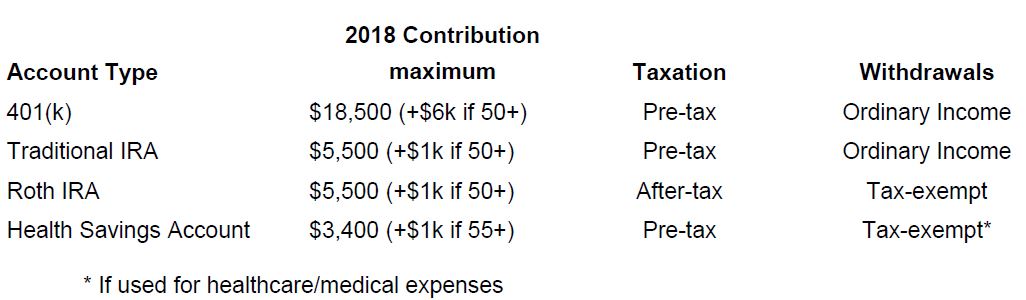

Clients often want to discuss ways to set aside more of their current income in a tax-efficient manner, in order to save for future retirement needs. They are mostly contributing the maximum to qualified retirement plans at work, or are using other available retirement vehicles that have lower maximum contribution limits, such as traditional or Roth IRAs. In some cases, the tax benefits of these retirement accounts are not immediate. However, the key goal is to build up a large enough pool of assets by the time you retire to support all of your cash flow needs through life expectancy. Combining different types of savings vehicles to meet future cash flow needs can result in a more effective tax strategy over time.

Healthcare is one of the largest expenses that individuals face in retirement. According to a Fidelity Investment study released in April of this year, a couple retiring today will need $280,000 over their lifetimes to cover health care premiums and out-of-pocket medical costs. Typically, clients think about covering those costs from the money they have accumulated in their 401k/IRA/qualified retirement plans. But there is another option that is often overlooked.

A Health Savings Account (HSA), funded with pre-tax contributions and allowed to grow on a tax-free basis, can provide a good supplement to income from your taxable and retirement investments. Unlike a Flexible Savings Account (FSA) that you have to use each calendar year or forfeit the balance, HSA contributions can accumulate in the account and be invested for growth over time. The current maximum contribution to an HSA is $3,400 per year for singles and $6,750 for families. You can contribute an additional $1,000 if you are age 55 or older. An added benefit is that you can withdraw from the account on a tax-free basis, as long as the funds are used to pay for medical expenses. So, you can earmark this pool of money to help cover the large healthcare bills later in life, without having to deplete other tax deferred accounts for that purpose.

In order to open an HSA, you must also enroll in a high deductible health insurance plan. You will want to carefully consider if that type of plan is best for you and your family in the near term. However, if you are relatively healthy and don’t visit the doctor often, other than for annual check-up type visits, and have the ability to pay the higher deductible if you need to, the long term benefits of the HSA can work in your favor.

A strategy that combines pre-tax and after-tax contributions and different tax implications on withdrawal may help best meet your retirement cash flow needs.

Please contact your relationship manager or the financial planning department if you would like to discuss the benefits of health savings accounts, or how to structure your retirement income.

______________

Registration does not imply a certain level of skill or training.

* Any conclusions presented or hypotheticals presented are based upon facts derived from publicly available information, and are also based on certain assumptions, including that there are no additional changes to current law, and that demographic information regarding retirement accounts also remains unchanged. Further, hypothetical scenarios presented are solely presented for the purposes of demonstrating available retirement options, and do not include any information, analysis, or conclusions regarding other areas of an individual’s financial future.

*Certain information presented includes facts and analysis the accuracy of which is dependent upon current regulations regarding taxes remaining unchanged. Changes in tax law or other rules could materially, and adversely, affect any financial or retirement plan. Therefore, no person reading this material should accept this information as investment advice.

*Some information in this presentation is gleaned from third party sources, and while believed to be reliable, is not independently verified.